Broad stock market rallies were a welcome sight at the start of the year, with the S&P 500 Index climbing 6.18% during the month of January. Bonds, in contrast to much of 2022, also gained value. Inflation slowly came down, although the Federal Reserve emphasized the continued need for higher interest rates to bring both inflation and the labor market into optimal positions.

Investors were digesting the potential for higher rates – trying to balance the risk of continued inflation with the risk of higher rates placing a dampener on economic growth.

Rumblings in the Banking Sector and Economic Implications

Of course, the world always has surprises, and March’s surprise was the failure of Silicon Valley Bank (SVB), the country’s 16th-largest bank. The reason for the failure was essentially poor risk management practices. SVB has long marketed itself as a bank for startups (risky), especially technology startups. Deposits rolled in for years as low interest rates helped create wildly profitable technology companies. That changed when the Fed started rapidly raising interest rates in 2022, triggering the “technology winter” of falling profits and rising layoffs. Technology companies, unable to secure cheap loans at low interest rates for funding, drew on their cash deposits at SVB. Meanwhile, the bank had invested much of these funds in long-term bonds – a standard banking practice. When SVB clients needed their cash, SVB had to sell off its bonds – many at large losses – to make cash available. At the end of the day, SVB was unable to meet the needs for available cash and became insolvent. The federal government worked with numerous banks to make SVB clients whole, and it was announced on March 27 that First Citizens Bank will purchase SVB and its assets.

Across the Atlantic, Credit Suisse, a much larger and more globally connected bank, had its own crisis. The dilemma kicked off when Saudi National Bank, the largest shareholder of Credit Suisse, said it no longer intended to provide financial assistance to the struggling bank. The departure of a major benefactor, years of declining profits, and recent large losses associated with poor investments had all called into question the bank’s solvency. In the end, the Swiss government brokered a deal to rescue the systemically important bank. UBS, another Switzerland-based bank (but much more profitable), purchased Credit Suisse along with its assets and liabilities. Although the issues surrounding SVB and Credit Suisse are largely company specific, they highlight the stress higher interest rates place on the global financial system. My prediction is that the crises associated with SVB and Credit Suisse will be catalysts for making banks much more conservative in their business practices. This could have both positive and negative outcomes. The main positive outcome is that more conservative banking practices should help reduce the likelihood of future banking crises. The negative outcome is that banks, to lower the risk of their overall portfolios, may choose to lend less; it may be difficult to find a bank willing to lend to startups. Without capital, new businesses cannot be formed, which could lead to lower economic growth.

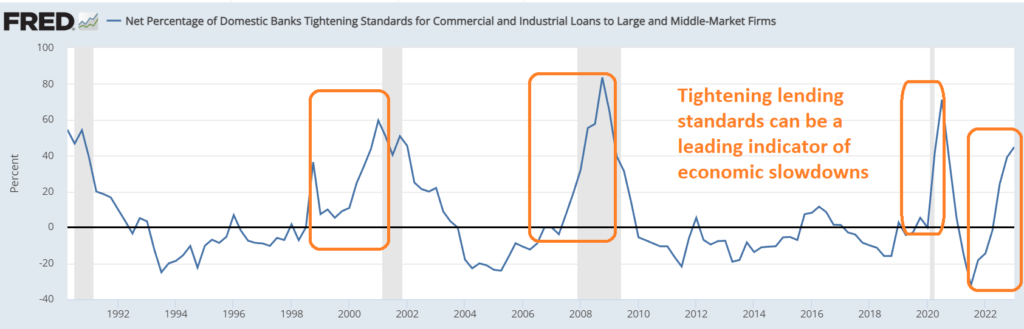

One indicator that I’ll be paying extra attention to is the Federal Reserve’s Senior Loan Officer Survey. Released quarterly (the next release is in May), this data details the percentage of banks that are tightening lending standards or turning away riskier loan applications. It can be a surprisingly good indicator of future economic growth, as tightening lending standards often precedes recessions. You can see below that banks have been steadily tightening lending standards since last year. I suspect the recent situation in the banking industry will only prolong this trend.

What About the Rest of the Economy? Inflation?

Sticky growth, sticky inflation. Our analysis had predicted rapidly falling inflation and economic growth into the first half of 2023. Instead, the economy has plodded along, with Gross Domestic Product increasing at an annualized 2.7% rate through the end of 2022 and the unemployment rate remaining near 50-year lows.

At the same time, the ongoing battle with inflation has run into extra innings. Month-over-month, housing inflation is still accelerating, and food inflation is still well above the Federal Reserve’s 2% annual target. For those who watch the news, the Federal Reserve is now paying less attention to the Consumer Price Index and more to Core Personal Consumption Expenditures (Core PCE), which is a better indicator of housing and services inflation. Still, there are pockets where inflation has substantially improved, specifically in manufactured goods and energy prices. Used vehicle prices, after climbing 56.3% post-pandemic, are down 13.6% over the last year. Similarly, gas prices have fallen from close to $5.00 a gallon to around $3.50. But, in Jerome Powell’s words, “the process of getting inflation back down to 2 percent has a long way to go and is likely to be bumpy.” In other words, expect higher interest rates for longer.

Our outlook for a broad economic slowdown is unchanged, though it may take until the second half of this year to present itself in the data. Forward-looking indicators, including supply-chain statistics, business sentiment, and market-based data, continue to support this outlook. As such, we’re still relatively conservative in our investing strategies, opting to invest in more defensive sectors and less risky types of securities (such as government Treasuries).

As always, we will be monitoring and adapting our investment strategies to new economic data and developments. If you have any questions, concerns, or would like to discuss your financial plan, our phone lines are always open at (561) 972-8011.

Christopher Diodato founded WELLth Financial Planning in 2020 to help individuals live their best financial lives through expert, conflict-free guidance. He carries a rare combination of credentials — the CFA, CMT, and CFP charters — allowing him to create and implement best-in-class investment and financial planning strategies. A passionate advocate of the FIRE movement, Chris helps clients design life plans that reflect their unique vision of financial success, whether that means early retirement or more time for what matters most.