2021 was the “COVID recovery” year for the economy, with industrial production, corporate profits, and gross domestic product all vaulting to new highs from their depressed 2020 levels. The unemployment rate, which peaked at 14.7% in April of 2020, dropped to 3.9% by the end of 2021. Trillions of dollars of government stimulus helped buffer the balance sheets of consumers, and demand for everything jumped.

Though demand was robust, supply chains were still struggling, and many industries (e.g., auto manufacturing, food service, and homebuilders) were hampered by shortages. Finding employees also became difficult and costly, as the size of the labor force remained several million people below its pre-COVID peak. The powerful consumer demand and scarcity of goods/services/labor caused inflation, as measured by the Consumer Price Index (CPI), to rise to its highest level since 1982.

Now, the Federal Reserve (colloquially known as “the Fed”), which is tasked with keeping unemployment low and prices stable, has made combating inflation a priority. To this end, they are planning on increasing interest rates and gradually reducing the money supply (they increased it greatly in 2020 and 2021 to stimulate the economy). It is expected their target “Federal Funds Rate” range will increase from 0.00%–0.25% to 1.00%–1.25% by year end.

What Happened Last Time the Fed Raised Rates?

The last period the Fed increased interest rates was from Dec. 2015 to January 2019. During that time:

- The Federal Funds Rate increased from 0.00% to almost 2.50%

- Some savings account rates increased to 2.50%

- Economic growth remained stable

- The S&P 500 climbed 37% (includes dividends)

- Mortgage rates fell slightly

- Car loan rates increased from about 4.50% to 5.35%

- The Barclays Aggregate Bond Index climbed close to 7% (includes interest payments)

That last bullet highlights that the Federal Reserve increasing interest rates doesn’t mean bond investors will necessarily lose money and highlights a question many investors are asking right now, which is:

Why Own Bonds When the Fed is Increasing Interest Rates?

Higher interest rates dampen bond returns since higher yields on new bonds make previously issued bonds with lower rates unappealing. So why own bonds at all? The Federal Reserve only sets the Federal Funds Rate, which is a very short-term interest rate (in fact, it’s an overnight interest rate stated as an annualized percentage). Other short-term interest rates (1-year Treasuries, savings account rates, rates on lines of credits, short term corporate bonds, etc.) tend to move in lockstep with the Federal Funds Rate. Longer-term rates (5+ year corporate bonds, 5+ year Treasuries, and mortgage rates) may be influenced by Federal Reserve policy but also move based on economic growth and inflation expectations.

From 2016 through the end of 2018, the Fed increased the Federal Funds Rate from 0.00% to nearly 2.50%. Meanwhile, the 10-year Treasury climbed from 2.25% to about 3.00%, a less significant rise. Some may ask, “But any interest rate increase will make bond funds lose money, right?” Not necessarily. An investor in a 10-year Treasury fund would have earned about 3.75% over this period because, while rates were slowly rising, the bond investor was still earning interest at a higher rate than by simply owning short-term bonds. The interest can provide a loss buffer when rates are rising.

Even so, a 3.75% return over three years barely sparks excitement, so why else would one own bonds in a rising rate environment? History strongly supports that bonds, and specifically longer-term Treasury bonds, are the ultimate diversifier of stock market and economic risk. With few exceptions, when stocks do poorly, Treasury bonds perform well. This is why a 60% stock (Vanguard S&P 500 Index Fund) / 40% intermediate term Treasury (Vanguard Intermediate-Term Treasury Fund) portfolio only fell 17.8% during the 2008 economic collapse while a 100% S&P 500 portfolio dropped by 37.2%. We can’t be completely sure how the economy will fare in any given year, but the evidence supports bonds as a convincing hedge against stock market and economic risk, regardless of what the Federal Reserve is trying to accomplish.

Stocks & Rising Rates: Valuations May Matter Again

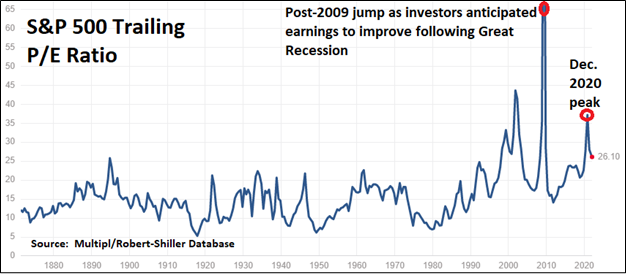

The S&P 500 “price to earnings (P/E) ratio,” which is a tool to measure whether stocks are over- or undervalued, remains well above its historical average (it’s currently around 26 versus its average of 16), suggesting overvaluation among stocks. It was as high as 39 in December 2020, but the reading was largely based on investors expecting earnings to catch up as the COVID-shuttered economy recovered.

What’s our take? Stocks are overvalued, and, for this reason, we expect stock returns to be lower over the foreseeable future. This overvaluation has been somewhat tempered by lower interest rates, but rates are going to be increasing again. When interest rates are higher, people are less willing to buy overvalued stocks since they can earn relatively more on less risky bonds. That’s why the S&P 500 P/E ratio fell to single digits during much of the 1970s.

In our opinion, higher interest rates could prove a headwind for the broad market—but not materially until 2023 since higher interest rates take several months to start impacting the economy. We believe unprofitable upstart technology companies and the private equity sector (think “home-flipping” but with entire businesses) could stumble sooner, as they rely heavily on low-interest debt financing. For us, we’re sticking to high-quality companies across multiple market sectors.

Final Thought – When Will This High Inflation End?

Inflation over the last year was driven by both very high consumer demand (because of stimulus and higher savings during 2020 lockdowns) and restricted supply (due to supply chain issues and periodic COVID spikes). We can’t speak to when the supply side of the economy will normalize, but higher rates should begin to bring demand back to normal.

Our base case is that inflation is close to peaking. In recent Beige Book surveys conducted by the Federal Reserve, mentions of shortages are beginning to decline. Similarly, waning effects from stimulus (such as the increased child tax credit, which was discontinued in December) should contribute to demand normalizing.

What could change this outlook would be a revival of Biden’s $1.75T Build Back Better plan. The apparent last hope of this bill passing was quashed when Senator Joe Manchin (D-WV) gave a firm ‘no’ in December, but we still view a surprise deal in 2022 a possibility. Such a stimulus would serve to raise overall demand, something that would increase economic growth but also likely spark higher inflation.

The bottom line is the Federal Reserve is going to be increasing short-term interest rates this year. Their task is difficult—increase rates enough to reduce inflation without hurting the economy. We expect inflation to begin falling in the spring and longer-term interest rates to stay level or climb modestly. Stocks should generally fare well, but unprofitable, highly leveraged companies may struggle.

As always, we are here to help you with your financial planning and investment needs and can be reached at (561) 972-8011.

Christopher Diodato founded WELLth Financial Planning in 2020 to help individuals live their best financial lives through expert, conflict-free guidance. He carries a rare combination of credentials — the CFA, CMT, and CFP charters — allowing him to create and implement best-in-class investment and financial planning strategies. A passionate advocate of the FIRE movement, Chris helps clients design life plans that reflect their unique vision of financial success, whether that means early retirement or more time for what matters most.