The years 2021 and 2022 marked the highest inflation rates observed in over forty years and a surge in vehicle prices, both new and used. Even now (2023), with peak inflation in the rearview, new cars are approximately 21% more expensive and used cars 55% more than before the 2020 COVID pandemic.

To offset the lower affordability for vehicles, banks and car dealers are now offering longer-term financing options than traditional 24- ,36-, and 48-month loans. Nowadays, it’s possible to apply for car loans with terms of 72, 84, and 96 months. The way longer loan terms improve affordability is that they require lower monthly payments. For instance, a car loan for $35,000 at an 8% interest rate will have a monthly payment of $1,097 for a 36-month (three year) loan term but only a $494 monthly payment if the loan is spread over 96 months (eight years).

There are two main drawbacks to opting for longer loan terms. The first is that the overall interest paid over the life of a given loan will be substantially higher versus a loan with a shorter repayment period. The second is what I like to call the “negative equity trap,” which in effect can trap someone into owning their car for longer than they’d like.

The Negative Equity Trap Explained

Cars, like most things, lose value over time due to obsolescence and wear and tear. We’ve all heard the quip that a new car loses 10% of its value as soon as it’s driven off the lot – their value also declines between 15%-20% each year after. There are dozens of variables which can influence this, including make, mileage, accident history, and body type (I cover this in detail here), but that’s beyond the scope of today’s discussion.

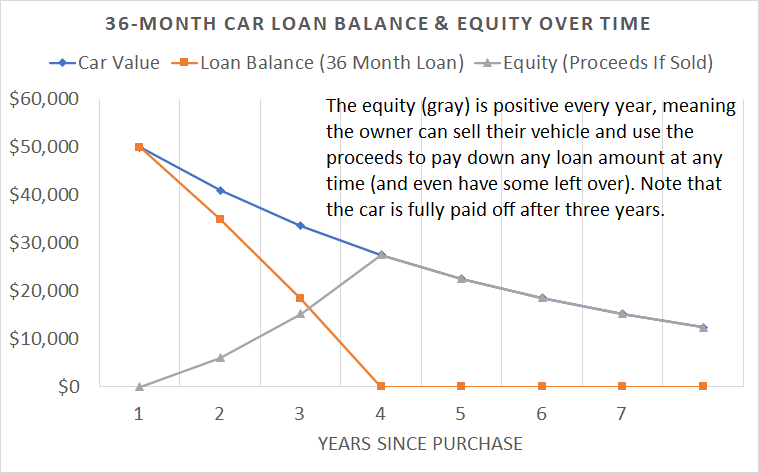

In an ideal situation, a car loses some of its value over time as you make your monthly loan payments. Should you want to sell the car before the loan is fully repaid, one can simply use the proceeds from a sale to pay off the balance of the loan, and maybe have some money left over.

In an opposite situation, which is common among cars financed with longer term loans, the vehicle loses value faster than the rate the car loan is being paid down. Therefore, if an owner wants to sell their car before the loan term ends, they will be responsible for paying the difference between the car’s sale price and its loan balance.

The charts below illustrate the idea of having positive equity (good) and negative equity (potentially bad) on a $50,000 with a 10% interest rate and an 18% annual depreciation rate in the car’s value.

Remember, this scenario has a $1,614 monthly payment, which would be considered unaffordable to many.

The monthly payment drops to $830 in the scenario above, but the owner will have negative equity for several years, meaning they will be unable to sell the car or get out from their payment should they want/need to unless they can come up with cash to pay the difference between the sale price and the loan balance.

Some concluding points we can draw from this analysis:

- Longer loan terms reduce one’s monthly payment versus shorter loan terms, which can make purchasing a vehicle more affordable.

- A longer-loan term will mean that more interest will be paid versus a shorter loan term.

- Negative equity means that the car’s value is worth less than its resale value. Negative equity is very common with vehicles financed with longer-term loans.

- If one intends on keeping their vehicle for several years, having negative equity during the first few years of a loan may not be an issue, since there’s no intention to sell the vehicle anyway

- Negative equity can present a major financial risk if one loses their income and can’t make their monthly payments, as there is no option to sell the car without incurring a large cash outflow.

- Longer-term loans are likely not suitable for people who like to buy new cars every few years. A lease may be the better option.

Christopher Diodato founded WELLth Financial Planning in 2020 to help individuals live their best financial lives through expert, conflict-free guidance. He carries a rare combination of credentials — the CFA, CMT, and CFP charters — allowing him to create and implement best-in-class investment and financial planning strategies. A passionate advocate of the FIRE movement, Chris helps clients design life plans that reflect their unique vision of financial success, whether that means early retirement or more time for what matters most.