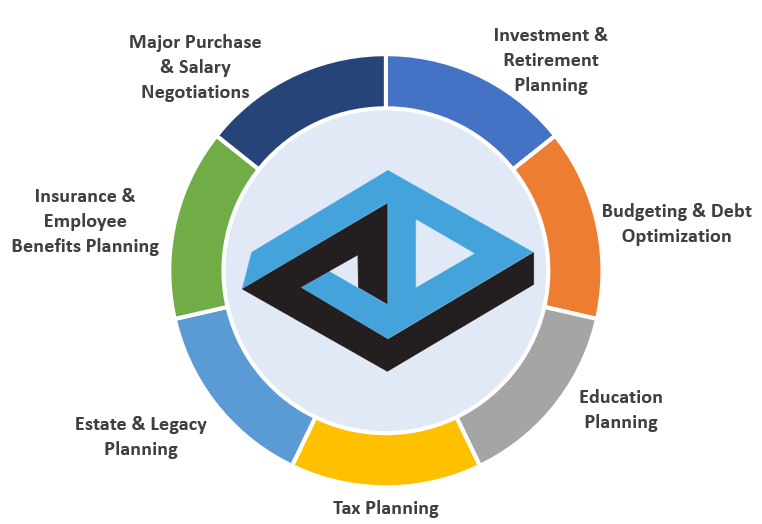

Is Financial Planning Worth It?

A financial planner is your personal concierge for all things financial. If it involves money, planners stand at the ready to make sure you are on track to maximize your wealth and hit your financial goals. Comprehensive financial planning, which is WELLth’s specialty, specifically leaves no stone unturned to reduce taxes, enhance your investments, optimize spending/debt, and protect your assets from financial and legal risks.

Who Benefits Most From Having a Financial Planner?

The chart here (click to enlarge) is from a blog post titled “Does Everyone Need A Financial Planner? No.” There, I explain that the people the value of hiring a financial planner increases with overall complexity of your financial picture. In simple terms, an individual with financial complexity may have:

- Lots of assets (homes, investment accounts, 401ks, CDs. trusts, business assets, etc.)

- Lots of debt (credit cards, car loans/leases, student loans, mortgages, HELOCs)

- Lots of family (spouse, children, grandchildren, older parents)

- Unique circumstances (multiple income streams, non-traditional retirement/work goals, business ownership/1099 engagements)

With that in mind, let’s dig into a hypothetical situation where we can quantify if it would be worth it for a family to hire WELLth as their financial planner.

Case Study: Mr. & Mrs. Angst

Mr. & Mrs. Angst know that their household finances are important, but money stresses them out. They have big dreams of being able to quit their corporate jobs and “work on their terms” by age 55. For them, this means buying and running an AirBnB for while taking summers off to travel to Europe with their two young children. They want to be sure they are saving enough for their dream, investing prudently, and taking positive steps now to minimize their lifetime tax burdens. They are ready and willing to what it takes to achieve this dream, but don’t know where to start and are worried about doing something wrong. No need to worry, WELLth is here to help!

The Angsts would receive a comprehensive financial plan which would serve as a road map to maximize their lifetime wealth and achieve their early retirement goals. This plan would include money-saving recommendations to implement over short-, intermediate-, and long-term timeframes. Some of these suggestions may include:

- Creating annual savings goals and budget recommendations in order to have enough funds for future years.

- Using special account types to defer paying taxes now at higher tax rates versus retirement.

- Fully utilizing benefits offered from employers to grow and protect. household assets.

- Refinancing high interest rate debt and working to improve credit scores for future major purchases.

- Insuring against a potential loss of income until enough savings are generated to self-insure.

- Creating strategies to qualify for low-cost health insurance during early retirement by minimizing recognized income.

- Formulating a plan to start the AirBnB business in the most cost-efficient manner, taking advantage of deductions and legal protections offered by different business types.

This is just a sample of the recommendations we may implement for a client. Even so, the recommendations above could easily make a six digit difference in lifetime wealth to the Angsts — a financial planning case well worth the fees.

What is not quantifiable is the peace of mind one obtains knowing a financial expert – a fiduciary – is working hard to make sure the Angsts achieve their best life. No more worries about making a mistake, no more anxiety about not saving enough to reach their long-term goals.

Quantifying the Value of WELLth's Recommendations

Every financial plan includes a side-by-side estimate of how much our recommendations will increase your net worth. This helps quantify the value of our tax-reduction, retirement, and investment strategies. In the majority of cases, we see expected six-figure improvements or more with our strategies versus how a client is currently going about their finances – an indication that the benefits of our recommendations often outweigh. our fees many times over

Is your financial life stressing you out like the Angsts? Want to see if hiring a fee-only financial planner can increase your net worth and lower your stress about household finances? Schedule a free phone consultation with us today.