President Biden announced last week a program to forgive $10,000 ($20,000 for Pell grant recipients) of student loan debt per person. To qualify for the forgiveness program, one must have student loans with the federal government (versus a private bank) and make under $125,000 per year. This means that a family filing their taxes jointly could make up to $250,000 per year to qualify. Speculation is that the government will use income figures from 2021 tax returns to determine eligibility.

That’s Great, But What About The Rest Of My Loans?

Regardless of whether you support the move politically, I always advocate taking free money when offered. It’s definitely a Rubicon moment for policymakers, however. It sets a precedent that executive orders to forgive student loan debt is now something that can happen! Because of this, and my personal opinion that the forgiveness action does not address the causes of the student loan crisis (crippling costs of college and high interest rates), I expect more forgiveness to occur in the future.

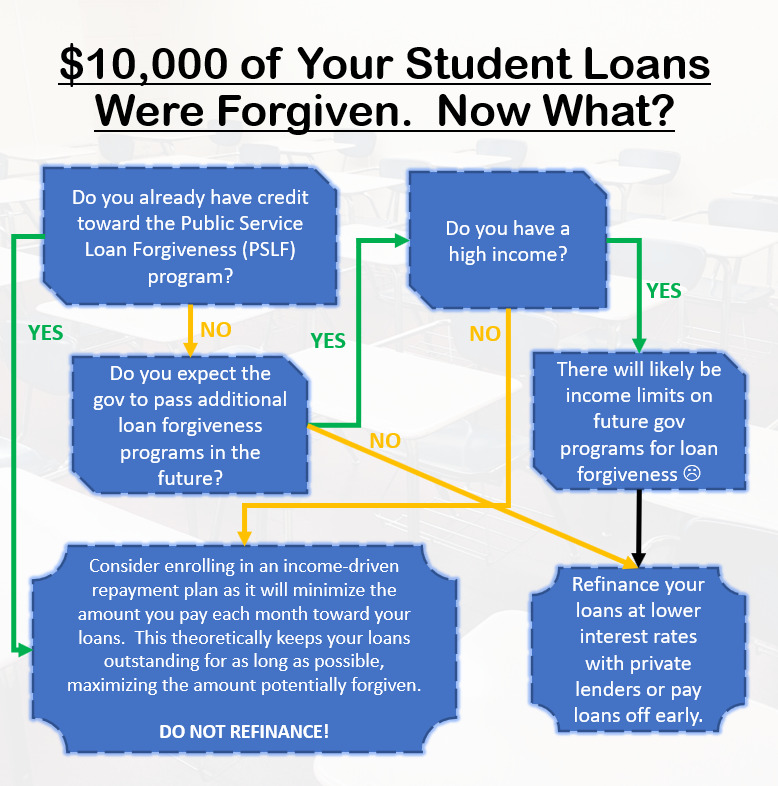

Do you agree? If so, there are some things you should and should not do to maximize the amount of your loans potentially forgiven. The advice is similar to what I give those trying to qualify for the Public Service Loan Forgiveness (PSLF) program which was passed in 2007. The advice? Minimize what you pay back to the government and don’t refinance. There are ways to to do this. For instance:

- Not paying down loans early

- Enrolling in income driven plans such as Pay As You Earn (PAYE) to lower your payments

- Maxing out retirement plans and tax-advantaged accounts such as 401ks, 403bs, IRAs, HSAs, and FSAs to reduce the amount of income used to calculate your payments

While I like the idea of minimizing payments, I don’t like the idea of long-term forbearance, as the balance of your loan will increase. In other words, it’s a risky move if forgiveness never happens. And don’t skip payments, we all work to hard to maintain our credit scores to do that.

And why shouldn’t you refinance? Unless your interest rate is exorbitant (over 10%, at least), the interest savings from refinancing with a private lender will pale in comparison to an amount potentially forgiven. It’s a risk-reward tradeoff. For example, would you rather save $2,000 of interest on a $50,000 loan over ten years or have a chance the entire loan is forgiven.

Anyway, here’s a flowchart to help with your decision making:

And, of course, if you have any questions about your specific situation, you can always shoot me a text at (561) 972-8011.

Christopher Diodato founded WELLth Financial Planning in 2020 to help individuals live their best financial lives through expert, conflict-free guidance. He carries a rare combination of credentials — the CFA, CMT, and CFP charters — allowing him to create and implement best-in-class investment and financial planning strategies. A passionate advocate of the FIRE movement, Chris helps clients design life plans that reflect their unique vision of financial success, whether that means early retirement or more time for what matters most.