Publix has become one of the Southeast’s most successful grocery store chains in history, operating 1,432 locations throughout the region and especially Florida. With net profits approaching $5 billion in 2025, the company clearly knows how to do business. These profits are shared with employees in the form of Publix stock grants through the company’s “Employee Stock Ownership Plan (ESOP).” Eligible employees receive up to 8% of their salary as Publix stock, giving them the ability to participate and enjoy the profits of the company in both the form of stock appreciation and annual dividends. Employees can also purchase additional Publix stock in their 401k SMART plan, but these purchases must be made with the employee’s own funds.

Peculiarities for Private Stock

Publix is a private company, and its stock is not traded on a major stock exchange, such as the New York Stock Exchange. Shares are also not available to be purchased by the public, unlike other well-known company stocks such as NVIDIA, Proctor & Gamble, and Exxon.

Because of this, shares are priced only four times per year. This brings in some opaqueness in terms of monitoring the company’s performance, but Publix has a long-track record of delivering excellent shareholder returns. More specifically, Publix stock has typically either matched or outperformed the broader stock market (using the S&P 500) for much of the last fifteen years. Performance has lagged the broad market recently, but this has been due to extraordinary returns from the large, AI-centric companies globally.

Because of the private nature of Publix stock, sales and distributions are a little more involved than placing a simple sell order online and waiting for a check. In fact, Publix requires mailed in distribution forms to request any distribution from an existing ESOP account.

Rules After Retirement

Publix has its own rules pertaining to its stock and retirement programs. The most impactful rule pertains to those who are either retired or otherwise separated from service. An ex-Publix employee must distribute their 401k SMART and ESOP plans at age 62 into an IRA or other brokerage account. This rule does not apply to current employees.

The consequences of this rule can be major, especially for those with large holdings of Publix stock. For these individuals, they face a major decision that can significantly impact their lifetime income and taxes during retirement.

Option #1 – Roll Assets Into an Individual Retirement Account (IRA)

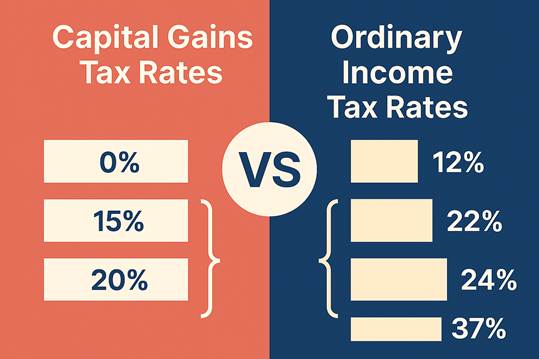

This option is the most straightforward, and the default method of choice for most individuals with a 401k. In this scenario, an ex-employee can move their assets to an IRA, either with Publix or another mainstream broker (e.g. Fidelity, Schwab, etc.). There are no immediate tax consequences of the rollover, but all future distributions will be taxed at “ordinary income” rates. This means the federal income tax rate would be the same as if one was simply earning wages from work.

There is another set of tax rates that apply to what’s called “capital gains.” These rates are typically lower than ordinary income rates, but do not apply for IRA distributions.

Finally, IRAs are subject to “Required Minimum Distributions,” meaning an account holder must begin taking account distributions at age 73.

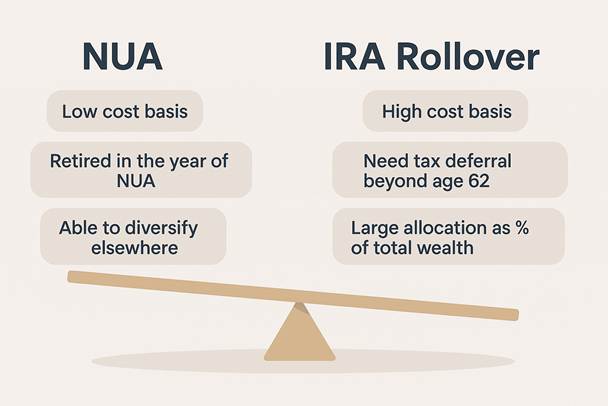

Despite the tax treatment, there is a major benefit of rolling a Publix retirement plan into an IRA – diversification. The Publix SMART plan has relatively few investment options and a long-time employee may have an excessive amount of their wealth tied up in Publix stock. Rolling over an account to an IRA immediately opens the investor to additional investment opportunities and chances to diversify without any tax consequences.

Option #2 – Net Unrealized Appreciation

Publix employees are afforded another option to distribute their Publix stock. This option is called a “Net Unrealized Appreciation (NUA)” distribution. Unlike an IRA rollover, this strategy transfers the entire account balance to a non-retirement account. The potential benefits of this strategy largely pertain to taxation and specifically converting a portion of the taxes to preferable capital gain rates instead of ordinary income rates.

In practice, the way this works is as follows:

- An employee transfers their Publix stock to a Publix brokerage account

- The entire “cost basis” is recognized as income in the year of the transfer and is paid at ordinary income rates.

- This typically results in a very large one-time tax bill for the employee.

- Cost basis can be retrieved by calling Publix HR at (863) 688-7407.

- From here, you can start making sales, but your gains will also be taxed.

- Appreciation beyond the cost basis is taxed at preferential long-term capital gains rates.

- Tax rules are tricky here as to whether there are holding periods to qualify for long-term capital gains treatment. Usually all appreciation at the date of the NUA is taxed as long-term capital gains while all additional appreciation will be considered short term unless shares are held for an additional year.

There are three requirements to execute an NUA strategy:

- The distribution must be made after a “triggering event, such as:

- Turning age 59.5

- Separating from service

- Death/disability

- The ESOP or retirement plan must make a total distribution of the account. In other words, the entire balance of the ESOP must be depleted after an NUA distribution.

- The shares must be transferred as-is to a taxable brokerage account.

- In other words, selling Publix stock and transferring the cash proceeds to a brokerage account will not qualify for NUA treatment.

Tax Benefits of NUA

By converting your gains in Publix stock to capital gain tax treatment, you can pay 20%, 15%, or even 0% in taxes when making sales. To minimize your overall tax burden, we recommend coordinating with a financial professional, as there are usually lots of other moving parts to consider (e.g. Social Security, Medicare, health insurance, fluctuating tax brackets).

Also worth considering is the initial “tax bomb” incurred in the year of making the NUA. Depending on one’s cost basis, this can launch an individual into some of the highest tax brackets. A careful analysis of the tax benefits of NUA versus the drawbacks of the one-time tax hit needs to be considered.

The Bottom Line

Whether in the 401k or ESOP, an NUA distribution usually makes sense when the cost basis of someone’s stock is low relative to their total stock holdings. Moreover, if one is still working at age 62, the NUA becomes less attractive since the taxes on the cost basis will likely be paid at higher brackets. In this case, an IRA rollover may be more appropriate.

We strongly recommend hiring an expert financial planner to help you make your NUA vs. IRA decision. A comprehensive financial plan can also give you guidance on how to maximize your diversification and minimize your tax burden in years after an NUA or IRA rollover. To schedule a call to begin your custom analysis and build a financial life plan, click here.

We hope this article was helpful and look forward to speaking with you soon.

Christopher Diodato founded WELLth Financial Planning in 2020 to help individuals live their best financial lives through expert, conflict-free guidance. He carries a rare combination of credentials — the CFA, CMT, and CFP charters — allowing him to create and implement best-in-class investment and financial planning strategies. A passionate advocate of the FIRE movement, Chris helps clients design life plans that reflect their unique vision of financial success, whether that means early retirement or more time for what matters most.